What Developers Need to Know About the Return of Chinese UHNW Capital

Chinese buyers are back in the market, but the rules have changed. Certainty now matters more than speculation, and brands matter more than ever. Developers who understand this shift will move first.

What Developers Need to Know About the Return of Chinese UHNW Capital

After several years of muted outbound activity, Chinese ultra-high-net-worth capital is re-entering the global real estate market with renewed confidence. According to Savills Global Research, buyers from Mainland China, Hong Kong, and the wider Chinese diaspora are once again deploying capital internationally, and branded residences are emerging as one of their preferred asset classes.

For developers, this shift signals more than a cyclical rebound. It marks a structural change in how Chinese UHNWIs evaluate real estate opportunities abroad.

Historically driven by manufacturing wealth and yield-focused investments, today’s Chinese buyers are prioritising certainty, brand trust, and lifestyle alignment. In a world shaped by geopolitical complexity and capital controls, branded residences offer something standalone trophy assets often cannot: operational clarity, global standards, and resale liquidity backed by a recognised name.

Savills notes that branded residential assets appeal strongly to Chinese buyers seeking safe offshore exposure without the friction of hands-on ownership. Hospitality-led management, consistent service quality, and professionally run rental programmes reduce risk, a critical factor for investors managing assets across multiple jurisdictions.

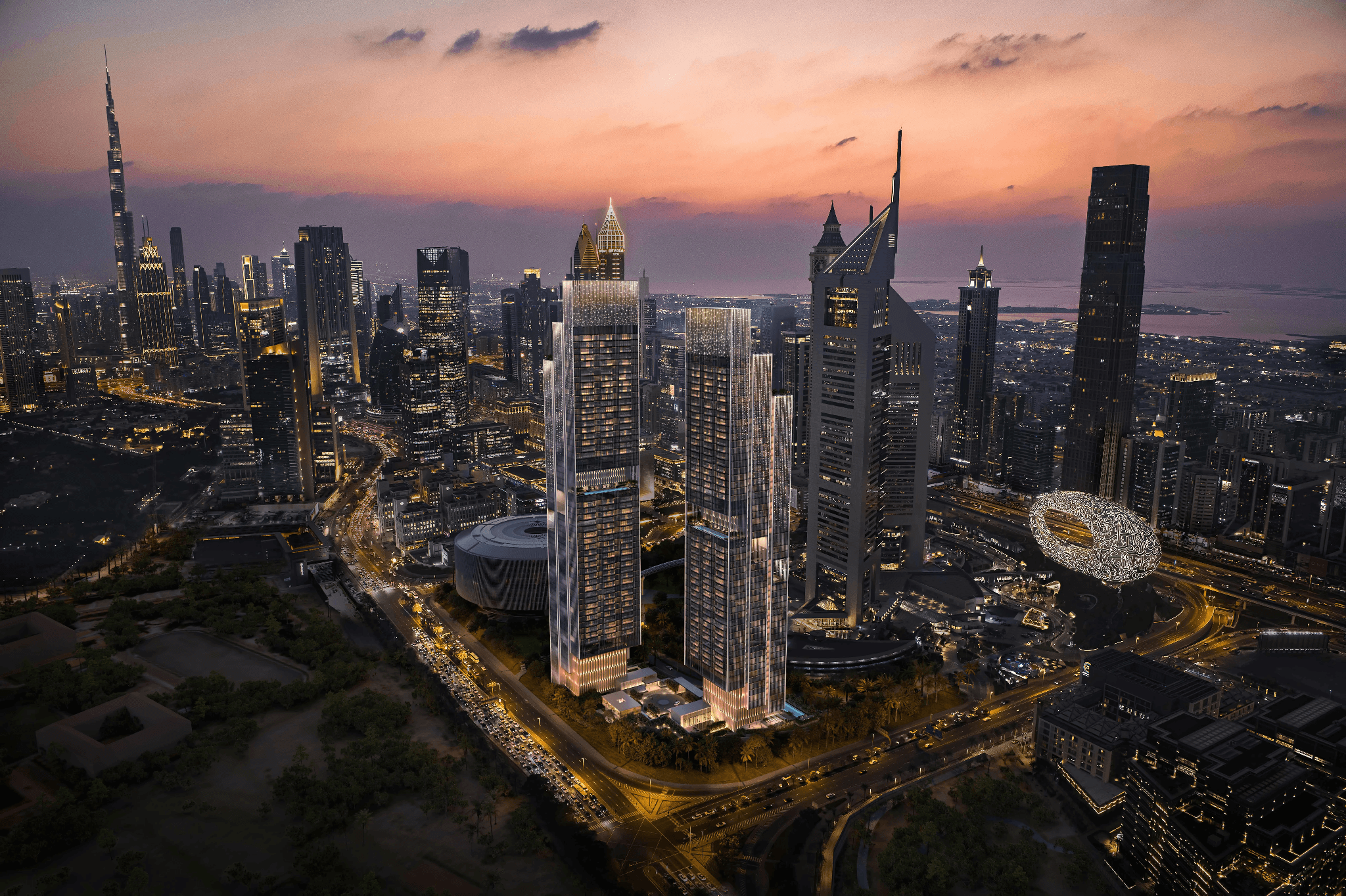

This demand is not evenly distributed. Capital is quietly concentrating in cities that offer mobility, education access, and long-term wealth preservation. Markets such as Dubai, Bangkok, Singapore, London, and Tokyo are benefiting from their openness, connectivity, and growing inventory of high-quality branded residences. These locations align with the priorities of next-generation Chinese UHNWIs: global lifestyles, family security, and intergenerational planning.

For developers, the implication is clear. Capturing this demand requires more than attaching a logo to a building. Chinese buyers are highly brand-literate and increasingly selective. They respond to projects that combine authentic brand storytelling, culturally fluent sales strategies, and amenities that reflect how they live, from wellness and privacy to concierge-driven convenience and global access.

Language capability, digital presence on platforms familiar to Chinese buyers, and partnerships with trusted international brokers are no longer optional. They are competitive necessities.

As outbound Chinese capital accelerates, developers who move early, with the right brand partners, locations, and execution models, will be best positioned to benefit.

In today’s market, branded residences are not just a premium product.

They are a strategic gateway to one of the world’s most influential buyer groups.

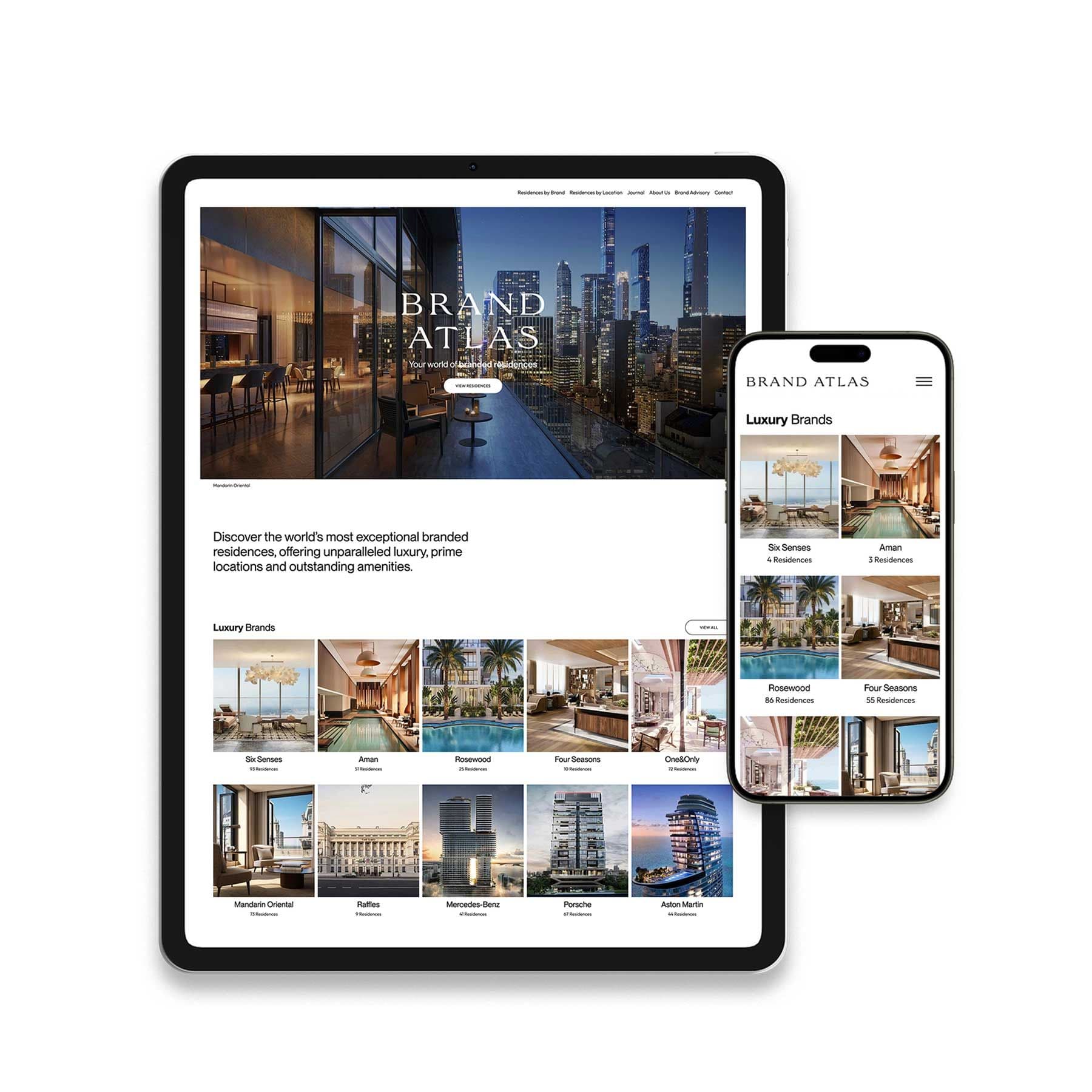

Brand Atlas is the world’s leading branded residences platform and brand consultancy.

Offering the definitive collection of the finest luxury branded residences in the most coveted locations, we give buyers and brands a unique opportunity to connect in this highly desirable and fast-growing market.

We work exclusively with leading brands, recognising the loyal relationship they share with their international audiences - and the exciting extension of luxury lifestyles through exceptional properties.

Providing an unparalleled and unbiased global overview, we enable buyers to see where their favourite brands are developing residences and to enjoy exploring and experiencing these exceptional properties.

Brand Atlas showcases the world’s finest branded residences on one digital platform, allowing global UHNW buyers access to a definitive collection of properties through a prestige network and top-tier technology.

Related News

The 10 Most Exclusive Branded Residences in 2026

In 2026, exclusivity in branded residences is no longer defined by price alone. It is shaped by a sophisticated combination of brand equity, geographical rarity, design integrity, and the ability to deliver a consistently elevated living experience.

Premium vs. Performance: The Real Trade-Off Behind Branded and Non-Branded Luxury

Paying 30% more for a branded residence is either a sound strategic move or an expensive oversight. What determines the outcome is not the name on the building, but how well the investor understands the underlying mechanics of the asset before they commit.

The Branded Residence Premium: How Much Is Real, and How Much Is Marketing?

In Miami, Dubai, London, and Singapore, a brand affiliation regularly adds 40% to the price of a residential asset over comparable non-branded stock. In prime markets globally, that range typically sits between 20% and 35%. Those numbers are real. They are also only half the story.