The Real Cost of Going Branded

The premium headline is well established. Industry research has found average price premiums of approximately 30% over non-branded equivalents in the same geographic market. The Savills 2025/26 report puts the global average at 33%, with resort locations reaching 39%. That number attracts developers into the category; however, it also has a tendency to mislead them.

The premium is real. So is what you are paying to generate it.

The Hidden Price of Luxury

Less visible costs, such as fees for maintaining shared amenities, brand-mandated design standards, and additional layers of brand oversight, can surprise buyers and increase complexity and expense. The same costs hit the developer's model long before they reach the buyer. Licensing fees, royalties, technical service agreements, and elevated specification requirements all add up at almost every stage of delivery.

Alignment and Operational Excellence

The premium pricing advantage depends on the service level and residential experience genuinely reflecting the brand promise, which requires operational excellence. When brand, product, and market are properly aligned, the benefits extend beyond price to include faster absorption, stronger buyer confidence, and better resale performance. When alignment is missing, the cost structure remains while the premium softens.

A Shift Toward Long-Term Durability

Industry leaders are stressing that the conversation has shifted from whether branded residences work to how to ensure their long-term durability through disciplined execution, transparent governance, and rigorous partner selection. In a market Savills projects will reach nearly 1,750 schemes globally by 2032, that discipline is no longer optional.

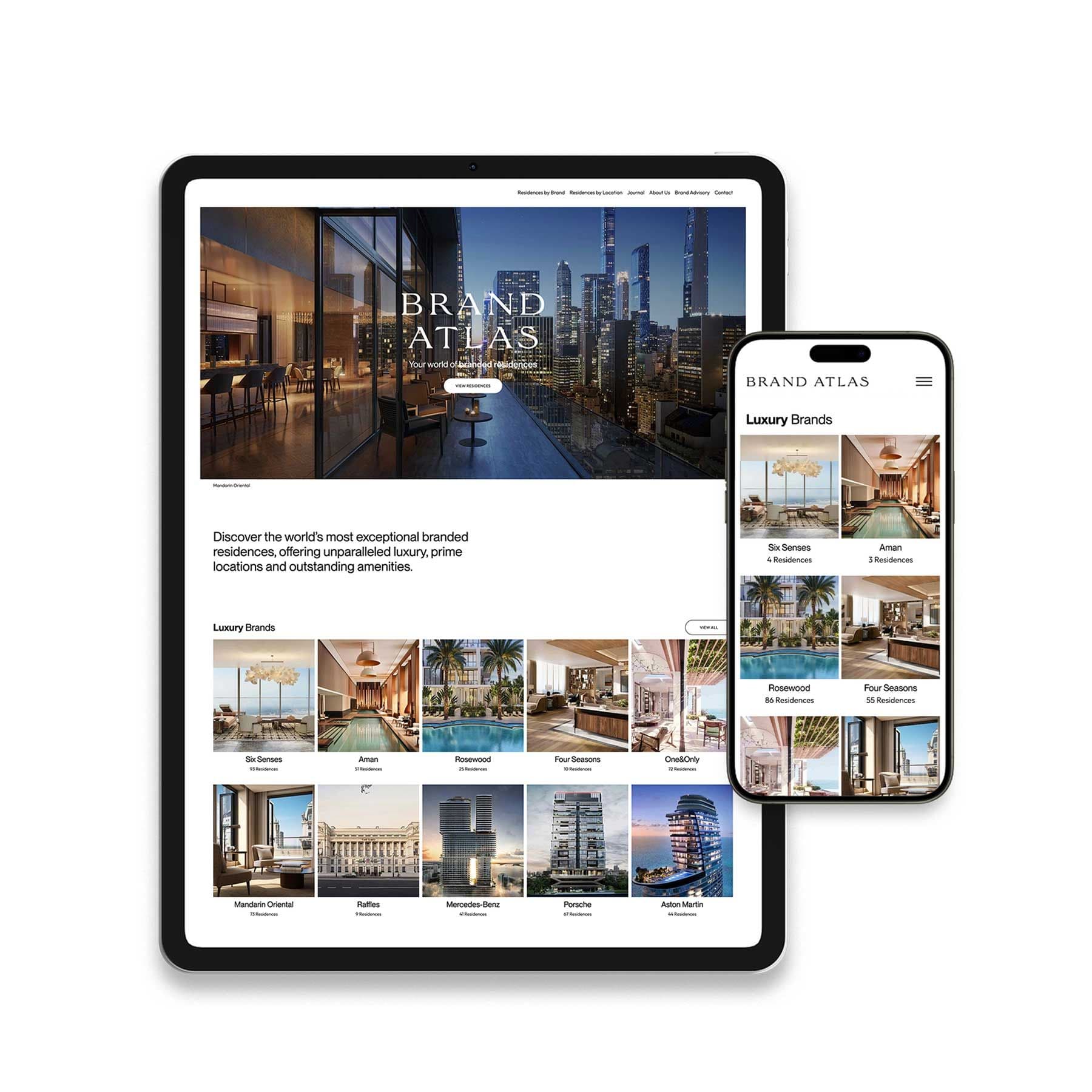

Brand Atlas is the world’s leading branded residences platform and brand consultancy.

Offering the definitive collection of the finest luxury branded residences in the most coveted locations, we give buyers and brands a unique opportunity to connect in this highly desirable and fast-growing market.

We work exclusively with leading brands, recognising the loyal relationship they share with their international audiences - and the exciting extension of luxury lifestyles through exceptional properties.

Providing an unparalleled and unbiased global overview, we enable buyers to see where their favourite brands are developing residences and to enjoy exploring and experiencing these exceptional properties.

Brand Atlas showcases the world’s finest branded residences on one digital platform, allowing global UHNW buyers access to a definitive collection of properties through a prestige network and top-tier technology.

Related News

The 10 Most Exclusive Branded Residences in 2026

In 2026, exclusivity in branded residences is no longer defined by price alone. It is shaped by a sophisticated combination of brand equity, geographical rarity, design integrity, and the ability to deliver a consistently elevated living experience.

Premium vs. Performance: The Real Trade-Off Behind Branded and Non-Branded Luxury

Paying 30% more for a branded residence is either a sound strategic move or an expensive oversight. What determines the outcome is not the name on the building, but how well the investor understands the underlying mechanics of the asset before they commit.

The Branded Residence Premium: How Much Is Real, and How Much Is Marketing?

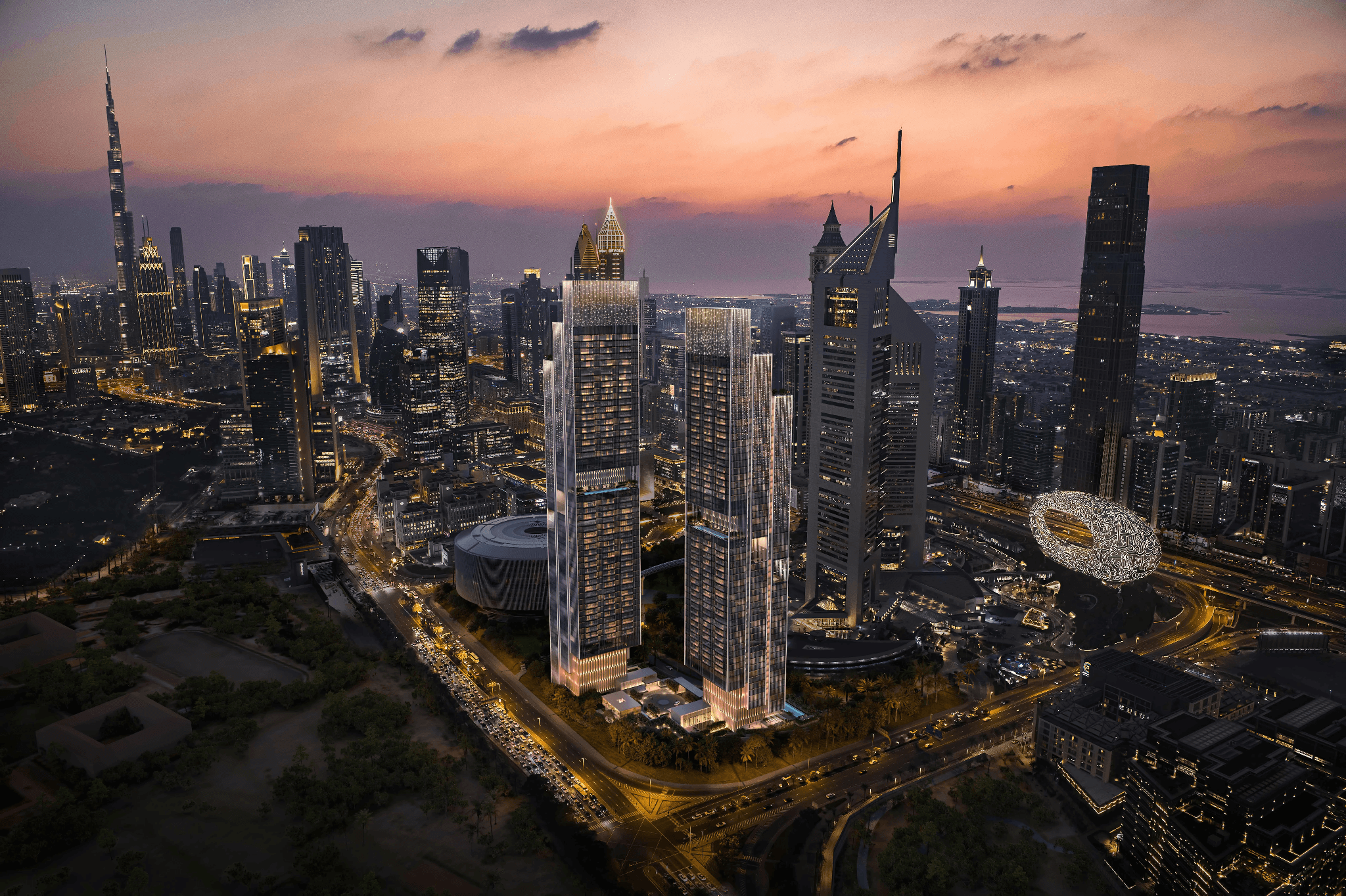

In Miami, Dubai, London, and Singapore, a brand affiliation regularly adds 40% to the price of a residential asset over comparable non-branded stock. In prime markets globally, that range typically sits between 20% and 35%. Those numbers are real. They are also only half the story.