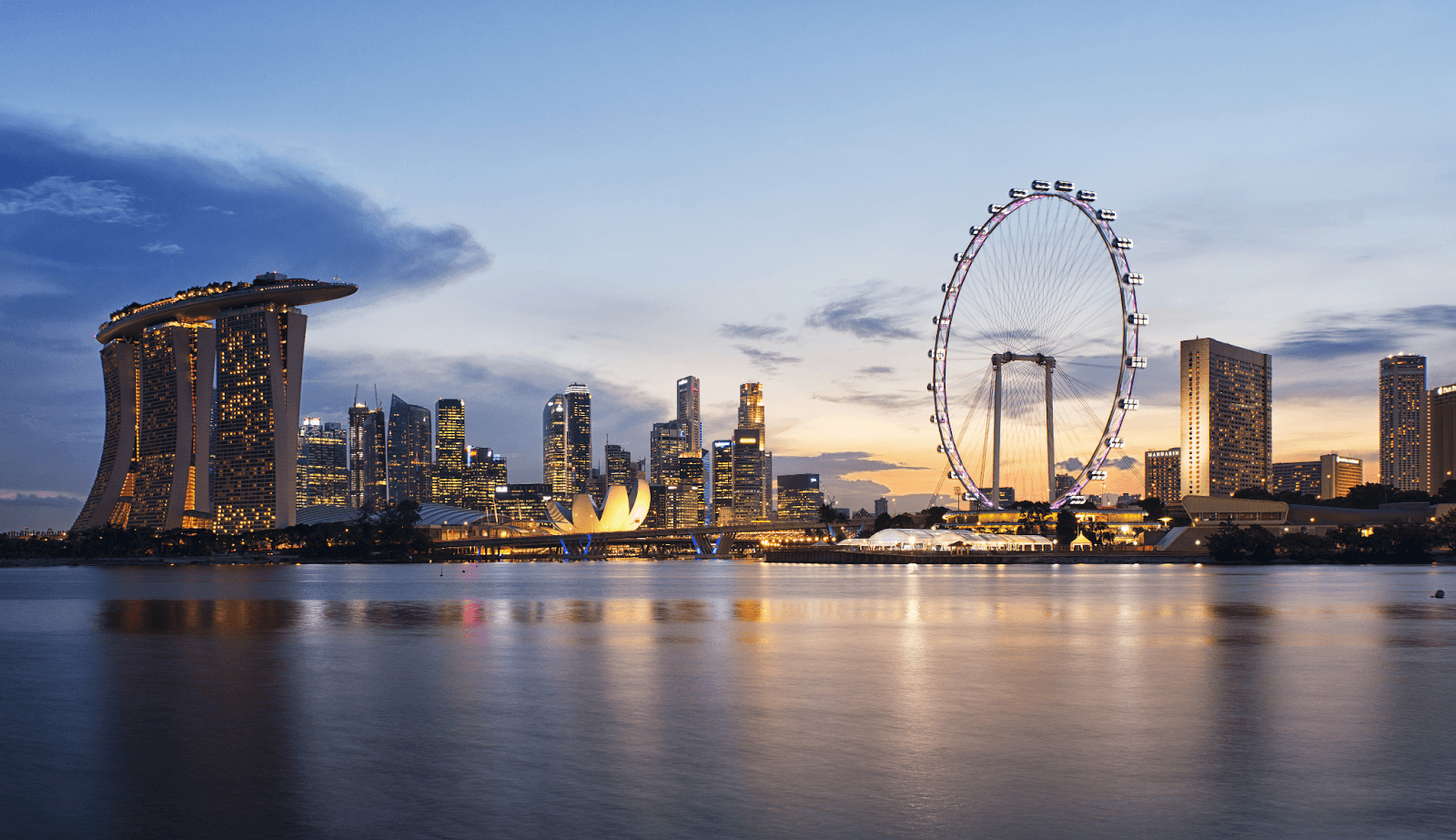

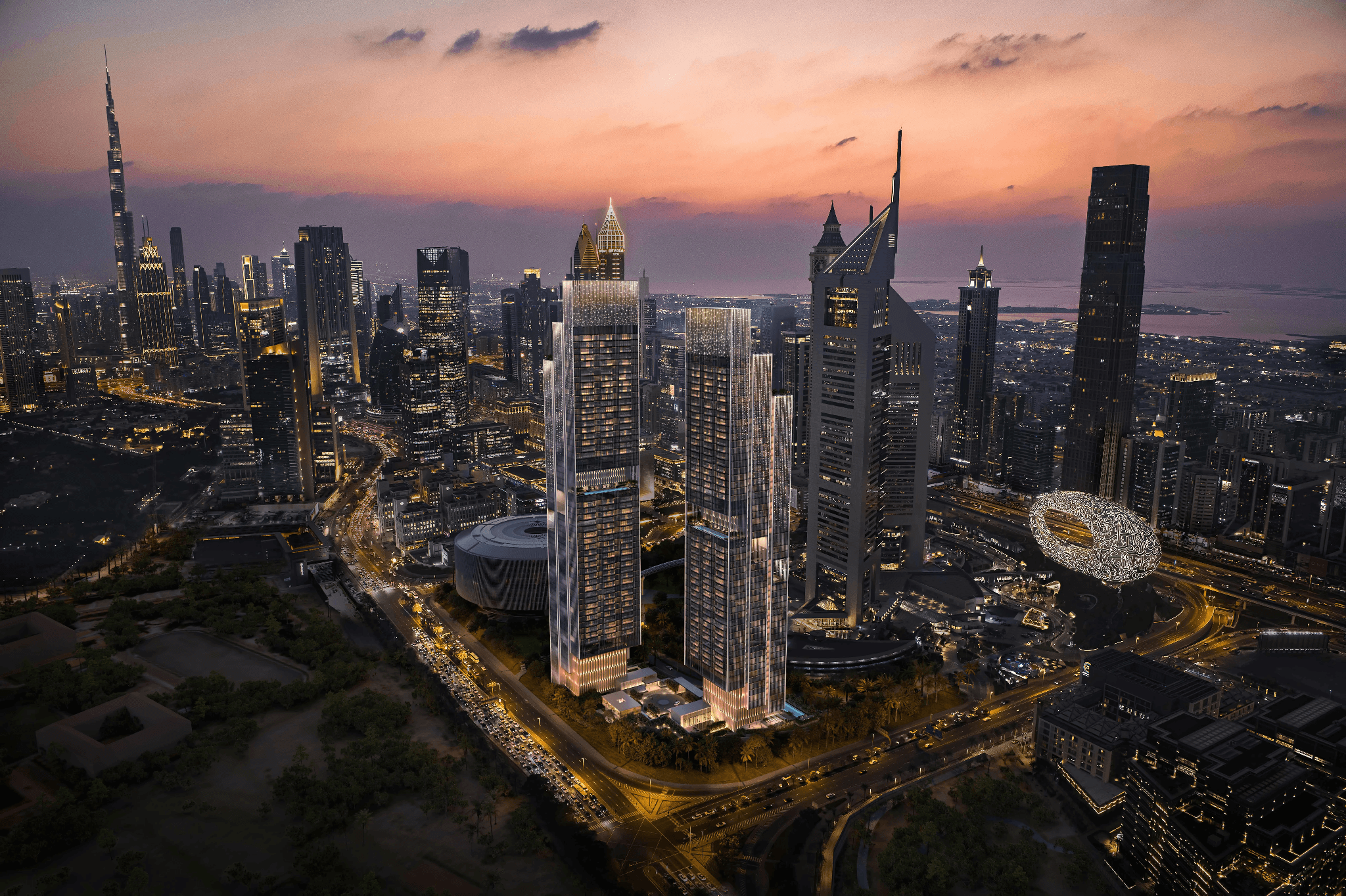

The "Fire Horse" Cities: Where Chinese UHNW Capital is Pooling Now

While the world watches for a rebound, Chinese ultra-high-net-worth capital has already made its move. Demand is no longer scattered; it is concentrated in five "Fire Horse" cities: Dubai, Bangkok, Singapore, London, and Tokyo. For developers, the win isn't just about location, but about "Brand Certainty." Projects that lead with professional operators and service-led design are capturing this demand before the competition even wakes up.

The "Fire Horse" Cities: Where Chinese UHNW Capital is Pooling Now

Chinese ultra-high-net-worth (UHNW) demand is returning to global real estate, but not evenly, and not loudly. According to the Savills Branded Residences Report, capital from Mainland China, Hong Kong, and the wider Chinese diaspora is quietly concentrating in a select group of globally connected cities. For developers, understanding where this demand is flowing is now as critical as understanding why.

Why These Cities Are Winning

Dubai, Bangkok, Singapore, London, and Tokyo share a rare combination of factors Chinese UHNW buyers increasingly prioritise: mobility, education access, political and economic stability, and long-term asset preservation. These are not speculative destinations, they are strategic bases for global living.

Chinese buyers today are less focused on short-term yield and more on certainty. They seek environments where assets are easy to manage remotely, protected by strong legal frameworks, and supported by professional operators. This is where branded residences play a decisive role.

Branded Residences as a Capital Magnet

Savills data shows that branded residences consistently outperform non-branded luxury assets in resilience, liquidity, and buyer confidence. For Chinese UHNWIs investing offshore, brand-backed developments reduce perceived risk through trusted standards, global service consistency, and clearer exit potential.

In cities like Dubai and Bangkok, branded residences also offer price accessibility relative to London or Singapore, creating a strong entry point for first-time international buyers. Meanwhile, mature markets like London and Tokyo continue to attract capital focused on wealth preservation and legacy planning.

What This Means for Developers

The opportunity lies in early positioning. Developers operating in these “fire horse” cities who align with credible brands, invest in service-led design, and tailor their offering to Chinese-speaking buyers are capturing demand before competition intensifies.

This goes beyond marketing. Language support, culturally aligned amenities, wellness infrastructure, and long-term management clarity are becoming decision drivers. Developers who treat Chinese UHNW demand as a strategic audience, not an afterthought, are gaining pricing power and absorption speed.

The First-Mover Advantage

Chinese capital historically rewards early-cycle markets. As outbound demand continues to normalise, these five cities are emerging as the first beneficiaries.

For developers, the question is no longer whether Chinese UHNW demand will return, but whether their projects are positioned to receive it.

Brand Atlas is the world’s leading branded residences platform and brand consultancy.

Offering the definitive collection of the finest luxury branded residences in the most coveted locations, we give buyers and brands a unique opportunity to connect in this highly desirable and fast-growing market.

We work exclusively with leading brands, recognising the loyal relationship they share with their international audiences - and the exciting extension of luxury lifestyles through exceptional properties.

Providing an unparalleled and unbiased global overview, we enable buyers to see where their favourite brands are developing residences and to enjoy exploring and experiencing these exceptional properties.

Brand Atlas showcases the world’s finest branded residences on one digital platform, allowing global UHNW buyers access to a definitive collection of properties through a prestige network and top-tier technology.

Related News

The 10 Most Exclusive Branded Residences in 2026

In 2026, exclusivity in branded residences is no longer defined by price alone. It is shaped by a sophisticated combination of brand equity, geographical rarity, design integrity, and the ability to deliver a consistently elevated living experience.

Premium vs. Performance: The Real Trade-Off Behind Branded and Non-Branded Luxury

Paying 30% more for a branded residence is either a sound strategic move or an expensive oversight. What determines the outcome is not the name on the building, but how well the investor understands the underlying mechanics of the asset before they commit.

The Branded Residence Premium: How Much Is Real, and How Much Is Marketing?

In Miami, Dubai, London, and Singapore, a brand affiliation regularly adds 40% to the price of a residential asset over comparable non-branded stock. In prime markets globally, that range typically sits between 20% and 35%. Those numbers are real. They are also only half the story.