Why Some Cities Work For Branded Residences, And Others Don’t: A Look At Thailand

In the high-stakes world of global real estate, Branded Residences have evolved from a niche luxury asset into a dominant force, particularly in Thailand, which now commands a massive 23.3% share of the Asian market. However, a stark divide is emerging between cities where these projects generate record-breaking premiums and locations where they falter. For Property developers, understanding this divergence is no longer optional; it is the difference between a landmark success and a costly failure.

In this guide, you’ll learn exactly why specific Thai cities support the branded model while others pose significant risks. Here is the critical framework you need to navigate Thailand's complex branded real estate landscape.

The Anatomy of Successful Branded Residences Hub

Not all locations are created equal. The data shows that success in the Branded Residences sector is highly concentrated in primary hubs that offer a specific ecosystem of infrastructure and lifestyle integration. Currently, Bangkok and Phuket rank 7th and 5th globally for branded supply, and their dominance is built on structural advantages that secondary cities struggle to replicate.

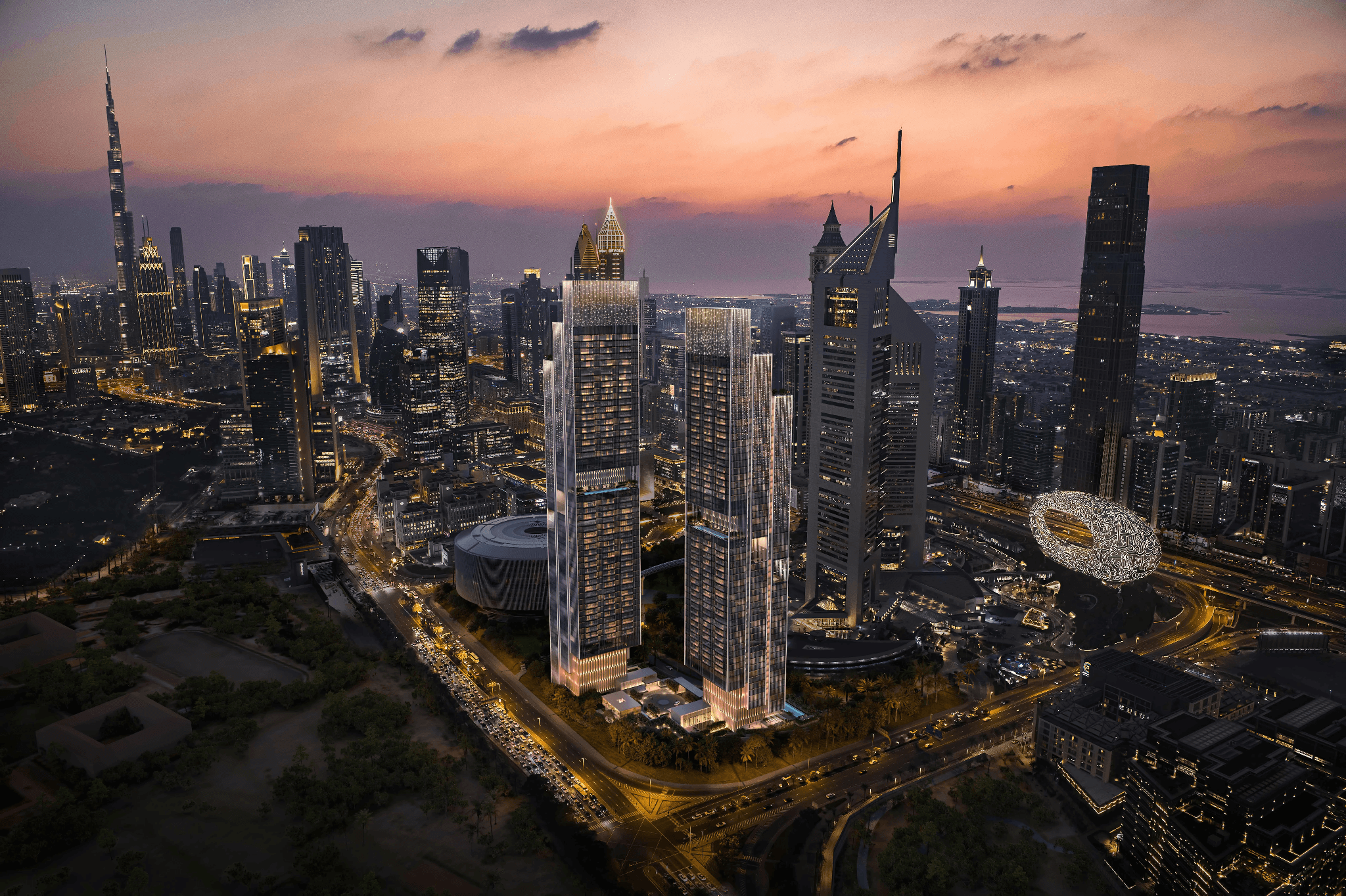

Bangkok: The Capital of Connectivity

In Bangkok, the branded model thrives on "mixed-use" synergy. Projects here do not exist in isolation; they are vertical cities integrated with Grade-A offices, luxury retail, and mass transit.

● Connectivity is Currency: Premium developments like One Bangkok or Dusit Central Park command prices exceeding $33,000 per sqm because they offer direct access to BTS/MRT lines and commercial ecosystems.

● The Service Necessity: The corporate elite and expatriates driving demand in Bangkok view 24/7 concierge services, security, and brand management not as luxuries, but as essential requirements for their primary residences.

Phuket: The Lifestyle Ecosystem

Phuket succeeds by functioning as a "hotel extension." Unlike urban condos, residences here are investment vehicles tied to global tourism engines.

● Global Reservation Systems: Owners leverage the distribution networks of giants like Banyan Tree or The Standard, turning holiday homes into high-yielding assets with 12–18% annual capital appreciation.

● Infrastructure Maturity: With international schools (UWC, BISP) and world-class hospitals, Phuket attracts long-term wealth, making "branded living" viable beyond just seasonal tourism.

The Risk for Property Developers in Thailand

While the allure of untapped markets is strong, secondary cities often lack the fundamental pillars required to support the premium price point of Branded Residences. Property developers venturing into these areas must navigate a "market mismatch" where the brand promise often exceeds the location's reality.

The Identity Crisis in Pattaya and Hua Hin

Pattaya and Hua Hin face a steep uphill battle due to fragmented market identities.

● Neighborhood Misalignment: A luxury brand like The Ritz-Carlton requires a surrounding neighborhood that reflects its prestige. In Pattaya, high-end projects often sit uncomfortably close to budget tourism zones, diluting the brand equity.

● Domestic vs. International Demand: Hua Hin relies heavily on domestic weekend tourism. This intermittent demand makes it difficult to guarantee the 5–7% net rental yields that international investors expect, compared to the year-round global draw of Phuket.

Moving Beyond "Logo-Slapping"

Even in a thriving city, a Branded Residences project can fail if the execution does not match the label. Property developers must recognize that sophisticated buyers now demand more than just a famous name on the door; they demand operational excellence and legal security.

1. EIA and Legal Deadlocks

In Thailand, Environmental Impact Assessment (EIA) is the gatekeeper of development.

● The Approval Trap: Many smaller developers market pre-sales before securing EIA approval. If rejected, the project stalls, trapping investor capital in legal limbo and destroying the developer's reputation.

● Regulatory Compliance: Navigating the complex zoning laws in resort areas requires deep local expertise, which international brands often lack without a strong local partner.

2. Management "Divorce"

A brand is only as good as its contract. The expiration or termination of a management agreement is a catastrophic value-killer.

● Case Study Warnings: Thailand has seen high-profile disputes where brands were removed due to failed contract renewals, causing property values to plummet overnight as residents lost access to hotel facilities.

● Agreement Durability: Successful projects require strong agreements that align the brand's standards with the owner's committee for decades, not just years.

3. "Logo Only" Trap

The era of "logo-slapping" using a brand purely for marketing without delivering services is over.

● Service vs. Marketing: Ultra-High-Net-Worth Individuals (UHNWIs) can spot a "lifestyle-only" brand immediately. They are shifting capital toward "hospitality-led" brands that offer tangible, hotel-grade services like in-room dining, housekeeping, and asset management.

● The Trust Deficit: If the service delivery fails to match the global standard of the brand, the premium paid for the property evaporates.

How Property Developers Ensure Long-Term Value

To succeed in this competitive landscape, Property developers must shift from a sales-first mindset to a value-first strategy. The market rewards those who treat branded residences as long-term operational assets rather than just construction projects.

Leveraging Professional Advisory

Navigating land strategy, brand selection, and market positioning requires specialized insight.

● Feasibility First: Conducting rigorous feasibility studies to determine if a location can truly support a specific brand tier is the first line of defense against failure.

● Brand Affinity: Developers must pair with brands that resonate with the specific demographic of the location, wellness brands for Phuket, and business luxury for Bangkok.

The Future of Branded Living in Thailand

The next wave of success will belong to projects that integrate wellness and sustainability.

● Green Tech Integration: Buyers are increasingly prioritizing eco-certification and wellness technologies.

● The Global Passport: Property is now viewed as infrastructure for life. Projects that offer "strategic living" proximity to education and healthcare will outperform those offering mere leisure.

Navigating the Future of Thai Real Estate

The divide between successful branded hubs and struggling secondary markets in Thailand will only widen as buyer sophistication grows. For Property developers, the lesson is clear: a brand name is an accelerator, not a savior. Success requires a deep alignment of location, infrastructure, and genuine hospitality operations.

Those who master this alignment will capture the major share of the Asian market, while those who ignore the fundamentals risk being left behind in a landscape that rewards excellence and punishes mediocrity. At Brand Atlas, we help you navigate this alignment, ensuring your development stands out in a competitive landscape.

Ready to capture the Asian market? Partner with Brand Atlas today.

Brand Atlas is the world’s leading branded residences platform and brand consultancy.

Offering the definitive collection of the finest luxury branded residences in the most coveted locations, we give buyers and brands a unique opportunity to connect in this highly desirable and fast-growing market.

We work exclusively with leading brands, recognising the loyal relationship they share with their international audiences - and the exciting extension of luxury lifestyles through exceptional properties.

Providing an unparalleled and unbiased global overview, we enable buyers to see where their favourite brands are developing residences and to enjoy exploring and experiencing these exceptional properties.

Brand Atlas showcases the world’s finest branded residences on one digital platform, allowing global UHNW buyers access to a definitive collection of properties through a prestige network and top-tier technology.

Related News

The 10 Most Exclusive Branded Residences in 2026

In 2026, exclusivity in branded residences is no longer defined by price alone. It is shaped by a sophisticated combination of brand equity, geographical rarity, design integrity, and the ability to deliver a consistently elevated living experience.

Premium vs. Performance: The Real Trade-Off Behind Branded and Non-Branded Luxury

Paying 30% more for a branded residence is either a sound strategic move or an expensive oversight. What determines the outcome is not the name on the building, but how well the investor understands the underlying mechanics of the asset before they commit.

The Branded Residence Premium: How Much Is Real, and How Much Is Marketing?

In Miami, Dubai, London, and Singapore, a brand affiliation regularly adds 40% to the price of a residential asset over comparable non-branded stock. In prime markets globally, that range typically sits between 20% and 35%. Those numbers are real. They are also only half the story.